What a year it's been. Crazy. And what a crazy year it already is so far. I haven't been posting much because there hasn't really been much to say. Like everyone else, I am doom-scrolling and wondering when this nightmare will end.

I have no particular view on how Covid will play out, so have no opinion whatsoever on travel and other hugely-impacted sectors. My guess is as good as anyone else's, so I have done literally nothing in my portfolio since this all started. In fact, I don't think I have even bought or sold a single stock in all of 2020.

So to just get that out of the way. And all these predictions about what the world would like like post-Covid, as usual, is all nonsense. Just filler material for magazines, newspapers etc. Nobody really knows. Some say we will return, eventually, to what we were before. Others say no way, we are not going back into offices and stores. But the truth will be somewhere in between.

Howard Marks

Anyway, I did notice a few things that made me want to make a post. One is that Howard Marks released a memo which was kind of stunning, I'm sure, for many value investors. His latest post, titled

Something of Value discusses the comparison between growth and value and even Bitcoin. He acknowledges that recent business models may justify higher valuations than in the past, and even goes as far as to withdraw, for the moment, his previous judgement on Bitcoin; he now says he doesn't understand it as well as he thought, so will refrain from making a judgement on it for now.

Buffett has always said that growth and value is joined at the hip, and Joel Greenblatt has explained that value investing is about buying something for less than it's worth, not just buying stuff that looks cheap on an absolute basis. So none of this is particularly new.

But I guess Marks jumped into the discussion because there is so much talk about mean reversion and markets going back to value. Within that context, I have said that even though there are cyclical tendencies that seem to go back and forth between growth and value, a lot of the recent widening of the gap may be due to dying industries; many industries are going to literally be obsolete. And on the other end of the spectrum is the different dynamics of the large, profitable tech businesses.

I saw record stores go away very quickly, even when people in the industry kept telling me that it won't go away so fast as people love physical CD's, liner notes, plus people hate waiting for their music to download. Apparently, some of these people didn't understand the exponential nature of technology. Book stores shouldn't exist either (and yes, book-lovers keep telling me that they can't read on their phones or Kindles; that they need real books to touch. This too will change. This is not to say that small, specialty bookstores can't survive and exist).

If you look around, and especially in the Covid world, you realize how the world is built around old technologies and capabilities. As Buffett says, if you were to rebuild something today knowing what we know now, and having the technology that we do now, would you build it the same way? (He actually asked if you would create the same company today from scratch, but close enough) Of course not. Think about that for a second, and you will see how much of what is in this world is obsolete.

Anyway, as I said, do you really want to be short AMZN and long BBBY? Well, OK, BBBY had a tremendous rally off the lows, and look at GME! Good thing I don't like to short things (and even if I did, I would never let a short go too far against me; I would cover quickly. I learned that lesson years ago. TSLA shows that many haven't learned that yet...).

Back in my more short-term-speculating days, we would take something like Marks' recent memo and pass it around as a capitulation of a great investor, sort of like Julian Robertson throwing in the towel in 1999/2000, or Stanley Druckenmiller flipping and going long tech stocks during that bubble.

My reaction this time, though, was that finally, he and much of the world is coming closer to my view. Which, of course, is sort of worrisome. I liked loving banks in 2011 when nobody loved them, and stocks pretty much all throughout this period as people kept calling this market a bubble.

Shiller

And then Shiller said recently that the market is not all that overvalued if you adjust it for real interest rates. I saw a chart of that somewhere, but can't find it now. I was going to paste it here, but I guess you can imagine what it would look like. It would look very different than the scary looking raw CAPE-10 charts.

I've been saying this for years, that even if we adjust long term rates back to 4% (from slightly over 1% now), that the market can be fairly valued at 25x.

I think I said something to the effect that, if, over the next decade, long term rates average 4%, I would not at all be surprised if the market P/E averaged 25x over that period. This means that the market can get up to 40x P/E in euphoric times and go down to 12x in panics. Remember, back in more 'normal' times, we thought that P/E's were normal at around 14x, and during bubbles, it went up to over 20x, and panic lows were around 7x P/E.

So that's all I'm doing. I'm taking what a future normal P/E ratio might look like and then giving it a high/low range based on what the market used to do around the average in the old days.

I know people argue that interest rates and earnings yields only correlated for certain parts of history, and hasn't done so in the longer term and in other countries. But I can't get around the fact that asset prices are largely determined by interest rates, so there should be a relationship.

Anyway, I think a lot of people are anchored to this idea that a normal P/E ratio is around 14x and think interest rates should be in the 6-8% range.

People often say that if interest rates tick up, we will no longer be able to justify these high P/E ratios. This is true. But again, we would have to see long term rates go above 4% for us to even worry about that. Sure, the market is going to tank if we get rates to 1.2%, 1.5%, or even 2.0%. Markets will react to that for sure. But, when that happens, keep in mind that ALL of my comments are assuming a 4% long term rate.

Singularity

By the way, I still recommend the same old books for investors, like

Security Analysis, but the book that may have had the most impact on me in terms of investing in more recent years might be

The Singularity is Near. I've owned this book for years but only read it in the past few years. This really explains what is happening in the tech world. When I read this, I immediately understood what is going to happen to a lot of businesses, so it helped me stay away from them, and made me appreciate the 'winner-take-all' businesses. The moat in this century is very different than the moat that Buffett talks about. Well, Buffett never restricted his definition of moats to old-world businesses.

Anyway, with a lot of challenges ahead, I don't know if these winner-take-all businesses will keep winning. There is a lot of pressure to rein in these folks, but I don't know how successful that will be. We don't want to kill the golden goose in this country.

Market Strong While the World Suffers

People talk about this all the time. With so much suffering, joblessness, starvation and death, the market continues to make new highs. Our nation's capitol is stormed and D.C. today looks like the green zone in Iraq. And yet, the market continues to make new highs. What's up with that?

Well, first of all, the odds of a 'coup' succeeding was always zero (let's not debate what you want to call that. I don't care either way). There was no chance a civil war would have started. The question was always just how many people are going to get hurt. So the market not reacting to that is not abnormal at all since the market reacts to future potential earnings and economic growth, which is still intact (whatever you expect).

And as for the economic, social and physical suffering in the world, when the government writes such huge checks, that money tends to go straight to the bottom line of a lot of companies. OK, maybe mostly to AMZN, WMT, COST, TGT and other big corporations. But guess what? Those big corporations are all listed companies, right? So small businesses (that are not listed) fail. Small restaurants go out of business. You want to eat out? Guess who is left standing? Yes, the national and international chains. So profits are moving from unlisted entities to listed entities. That is kind of huge when you think about it.

Look at CMG. I have been a fan for years, and have owned this for years (first purchase was in the $30s). Even I think it's nuts how expensive it is. But they are just taking market share, or soon will do so because of Covid. I know this is not permanent, and eventually things will go back to normal. But I wonder how much business will go back. If you are going to start a new business, who wants to open a new restaurant when insurers won't cover for pandemic closures? And who knows when the next one will come? Experts say that Covid-19 is not even the "big one" they are worried about.

Also, when there is stimulus where the government cuts taxes on the rich, a lot of those savings aren't injected back into the economy. Maybe they go into bonds or cash balances. Some of it will go to spending. Some go into real estate and other investments. But when you write checks to lower income folks, they are going to be more likely to spend a bigger percentage of that.

Well, having said that, I know there is data showing that a lot of that money actually didn't get spent, but went to pay down debt, savings, and some to Robinhood trading accounts, and probably into Bitcoin.

Renaissance Technologies

By the way, (and what's a Brooklyn Investor post without a random tangent / digression), people are wondering how the Medallion fund can return 70% while the institutional funds for outside investors are down 20-30%. Well, when they announced the new funds for outside investors, I knew it wasn't going to work, or wasn't going to be as good as the Medallion fund.

This is a very important point to keep in mind. The Medallion fund has such high returns and is much more stable because they do a lot more trades and analyze every anomaly with many more data points. I was once involved in HFT / stat arb, and we had tons of data to work with even from the past three months, as we had every single trade (tick data) for every single stock, or at least the listed stocks. That's a lot of data. With that kind of data, when you find an anomaly, you are going to have a very, very statistically robust way of testing to see if it is meaningful, and you will have plenty of opportunities to make those trades to actually realize that statistical edge. And when you do so many trades like that, your returns tend to get more consistent, which means that you can lever up, which further boosts your returns. Just imagine the lumpiness of your daily revenues in a casino with 10 slot machines vs. one with 10,000 slot machines.

Now, if you try to apply some of this to longer term data, say, daily data, you suddenly have a small fraction of data to deal with. And, to me, much more significantly, you are now dealing with data that the human eye can see (such as P/E ratios, opening and closing prices). Anomalies found in tick-data is invisible to humans, and only visible to machines that have access to the data and models that can process and analyze them.

Put it this way. If you use daily closing prices, there may be 253 prices per year. Over 100 years, that's 25,300 data points. Now, a fast model might use tick data, but let's assume you use prices from every second of the day. If there are 6.5 hours of trading per day, that's 390 minutes, or 23,400 seconds per day. So in one day, a stock can generate almost as much data as a 100 year history of a stock using daily prices. Go back 3 months and you see how much data you can work with. So when Renaissance says there is not enough data for their longer models, this is what they mean.

Looking at it this way, you see how silly the bubble-callers comments are. They are making predictions based on something that happened, like, two or three times in the past century (some include all the bubbles in history, but it's hard to compare other bubbles to the U.S. market). That's not a lot of data points to test the robustness of any claim you make.

So when people say, this is like 1929, 1987 or 1999, well, for it to be meaningful, you would have to have at least 30 of those events with the same variables at the same levels with most of them giving the same or similar results for it to be meaningful.

There was a famous quant fund that went belly up in the 90s, and it was shocking what kind of trades they were making. The analysis was something like, the last ten times this has happened, the market did this on average. It's like, what? You are going to make a prediction on only ten samples?! That makes no sense at all.

And yet, there are still plenty of people still making those sorts of predictions. They see that P/E's were over 20x in 1929, 1987 and 1999 so assume that every time the P/E gets over 20x, the market is going to crash. Or something like that. And then they line up all these valuations metrics to show how insane everything is when they are all actually showing a single metric as they are all related / correlated factors; any statistically robust, well-built model would assign most of them as a single factor. For a statistical model to be meaningful, input factors have to be uncorrelated.

The fast models used by Medallion (of course, I have no idea what they do, but do guess they are very fast models) and others use a lot of data and only make trades where there is a statistically meaningful chance that it will be profitable. And they will make enough trades for that statistic to play out. For example, if you have a 60% chance of success, but you are going to die because there is a 40% chance of death, then that's not a good bet. But if you can roll a dice that is 60% in your favor and you are allowed to roll it 100 or 1000 times, then that's a good bet. Odds are in your favor and you have enough opportunities for that statistic to be meaningful.

This is how casinos work. You want as many slot machines and gaming tables as possible, with as much capacity utilization as possible. With a slight edge in your favor, you can print money.

People who try to forecast the markets with flimsy models using very few data points is like a guy trying to run a casino with one or two slot machines, and wondering why he is getting killed. Well, most of them don't even have the odds in their favor as they haven't even calculated that correctly.

By the way, digressing from a digression, this is the same reason why most technical analysis is garbage. Books will show you all these amazing crashes following trendline breaks, head and shoulders tops and bottoms and whatnot, but they never show you the patterns that didn't work out. How many trendline breaks didn't lead to a crash? If you can't answer that question, then it is totally meaningless. Early in my career, I spent entire days and nights sitting in front of a computer (for one of the top hedge funds) trying to validate everything I was reading in books about technical analysis, and was unable to validate any pattern; needless to say, everything was random!

So next time you hear someone give you this technical baloney, ask them for data to prove it.

Anyway, moving on...

So, Are We in a Bubble?!

OK, so there is a lot of anecdotal evidence that there is a bubble going on. IPO's, SPACs, Robinhood trading, Bitcoin, just all sorts of stuff.

Sure, there is a lot of speculation going on, and there are a lot of things I would stay away from.

But at the end of the day, for me, as a stock investor, I just care about valuations. Is the stock market in a "historic bubble"? I don't know, but it doesn't really look like it.

With interest rates at zero, and negative real interest rates, and all this monetary AND fiscal pump priming, the market should be at 40-50x earnings. Well, I mean if this was a real bubble, it would be there. At that level, then yes, I would worry that we are in a bubble, and I would probably increase my cash position substantially (despite my "don't time the market!" stance). Even at over 30x, I would probably go carefully through my portfolio and dump stuff that is not 'reasonable'. Or I would do it in a more conservative way. Well, this is something that should be done every day anyway.

But now? It really doesn't feel that way to me. I am not predicting that we would get there, and I definitely would prefer it not do that as it would be quite a hassle. You could potentially be looking at decades of no returns from the stock market, like Japan. So I would want us to avoid that.

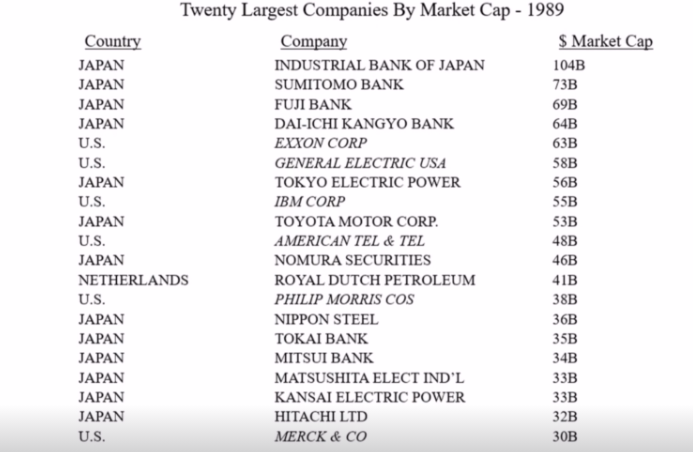

Speaking of Japan, the Japanese stock market hasn't yet recovered it's 1989 high. In that kind of bubble, yes, I would worry about owning stocks. But remember, P/E ratios back then were 60-80x for the whole market. That's too expensive to grow earnings into in a decade or even two, not to mention the government spending the first two decades preventing any restructuring etc... that would help the market recover. It was all about protecting / defending the status quo. Things seem to be changing slowly recently, though.

So, if we see that here (that kind of insane P/E), then yes, even I would start pounding the table to dump stocks, regardless of interest rates.

But I don't see that. In some places, yes, valuations are silly, but who cares? If you owned, say, BRK in 1999, who cares what the market valued Pets.com at? Just don't buy Pets.com!

This is another long post for another day, but there is hope even in a mega-bubble situation. We saw it in 1999 when reasonably priced stocks did really well through the bubble collapse. Even in Japan, I think there were some really good, solid, blue-chips that did really well after the bubble. Small and medium caps did really well too. So hopefully, there will be opportunities even in that scenario.

People constantly worry about 20-30% corrections. I don't worry about those at all, and I assume we will have a lot of those over even the next 3-5 years. I don't care about things like that too much. In fact, I don't even worry too much about a 1999-like bubble, because if you look back, if you owned solid, decent stocks and held on through it, you would have been fine. I expect the same going forward.

For me, I would only worry about a situation like 1989 Japan where things were so expensive that it might take years to work off the valuation, but even then, as I said, I would focus company by company and not worry too much about the overall market.